The full text of the Chancellor's 'Growth Plan' MiniBudget speech delivered by Chancellor Kwasi Kwarteng in the House of Commons shortly after 9.30am today.

As part of his ‘Growth Plan’ tax-cutting MiniBudget announced today the Chancellor has scrapped a planned rise in Corporation Tax.

In a surprise move today, Chancellor Kwasi Kwarteng axed the 45% Additional Rate of Income tax paid by 660,000 high earners.

The FCA is to carry out an extensive survey of solo-regulated firms to assess how they are coping with the cost of living crisis.

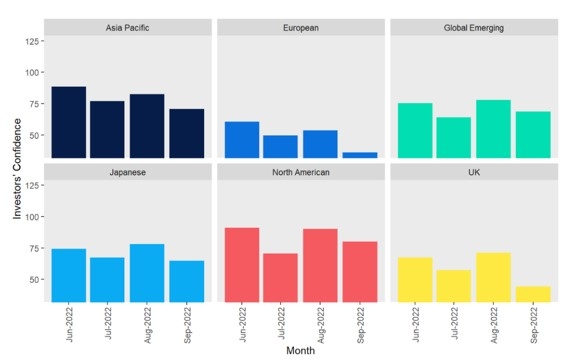

Confidence among investors is at its lowest level since May 1995, according to new data.

Financial Planners have shared their predictions for what will be included in today’s mini-budget from Chancellor Kwasi Kwarteng.

The Treasury confirmed this afternoon that it will scrap the 1.25 percentage point rise in National Insurance introduced in April.

The number of fund managers committed to net zero by 2050 has doubled to 81% over the past year but only two in ten (22%) have concrete carbon reduction plans, according to a new report.

The Chartered Insurance Institute has launched a Professional Map competency framework to help insurance and personal finance professionals develop their careers.

Annuity rates have risen by 35% over the past year to hit their highest point in a decade, according to a new report.